When Median Take-Home Pay Packets Only Rise Once a Generation for a Half-Decade Span: CHART OF THE DAY

We have built an economic régime where GDP climbs, markets soar, and the typical worker stands still unless the labor market is white‑hot. And if inflation fears keep us from ever running the economy hot again, real median wages may be stuck on pause indefinitely…

Ernie Tedeschi:

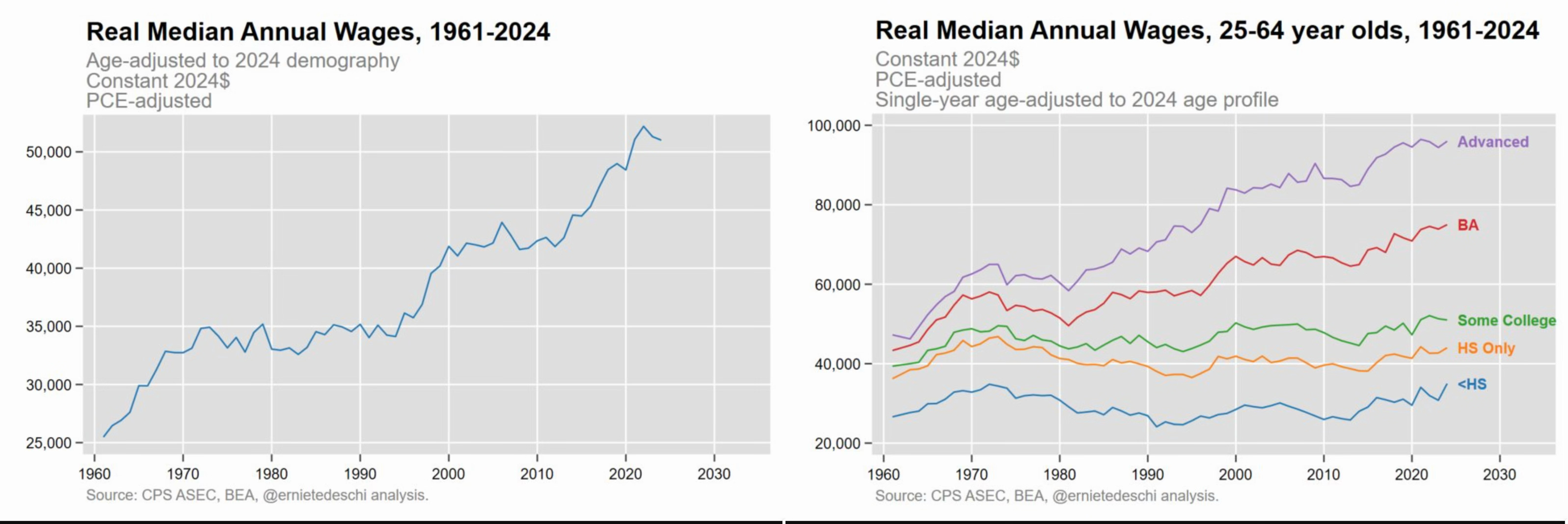

Ernie Tedeschi: <twitter.com/ernietede…>: ‘Once you sort through demographic change & use a consistent deflator over time, the story becomes more interesting: periods of stagnation to real median wages (1973-95, 2000-14, maybe now), followed by bursts of growth when we’re near full employment (1961-72, 1996-2000, 2015-22).

There’s real wage stagnation among workers with less than a BA, however the problem is that the type of worker who gets a BA or beyond is much, much broader now than it used to be. Successful workers have been increasingly sorting by education, and education in turn has an effect…

The way I was taught macroeconomics, there was a clean story. There was long-run growth—output per worker and thus living standards ratcheting upward at something like 2 percent per year—and then there were business cycles, with unemployment and output bobbing above and below that smooth trend. Wages, in that classroom story, were just the labor side of the same process: track productivity plus inflation and you have the typical worker’s paycheck. The path might be noisy, but the fundamentals were solid.

It is very hard to look at Ernie Tedeschi’s graphs and still believe that story for median real wages. Once you stop confusing “average” with “median,” stop confounding composition effects, and use a sensible price index, the picture that emerges is not “trend with cyclical wiggles.” It is long, flat stretches of stagnation punctuated by short, intense bursts when the labor market is genuinely, not performatively, tight.

Thus the post‑1960 U.S. experience for the typical worker has three, and only three, sustained episodes in which real median wages clearly and materially rose: pre-1968, the 1995-2000 boom, and 2013-2022.

The first is the long “golden age” up through roughly 1968: the tail end of the wartime and postwar social-democratic settlement, union density still near its peak, productivity growth fast, and the macroeconomic regime still oriented toward something like true full employment.

The second is the 1995–2000 boom, when Greenspan’s Fed, to its great credit, decided to run the economy hotter than almost any respectable model then said was safe, and was rewarded with falling unemployment, rising labor-force participation, and broad-based wage growth, especially toward the bottom.

The third is 2013–2022: the long, grinding recovery from the Great Recession that finally morphed into a genuinely high‑pressure labor market after 2015, and then, after the pandemic shock, the policy-driven turbo‑recovery of 2021–22 under very aggressive fiscal and monetary support.

Those are the only three periods when the median worker clearly and reliably pulls away from the starting line.

Everything else is—not great. Call the intervals in between the “Nixon–Ford–Carter–Reagan–H.W. Bush era,” the “W. Bush–Obama I era,” and what we might, with fingers crossed, call the “(so far) Trump–post‑Trump era.”

In these spans, aggregate GDP grows; the national average wage index that Social Security uses to update benefits, marches steadily north; the S&P 500 has a perfectly nice time. But the median full‑time worker’s real weekly pay mostly goes sideways. The old story—growth plus cycles—turns out to be a story about averages and totals, not about what happens in the middle of the distribution.

What jumps out is that a non‑high‑pressure economy is death to trickle‑down to the median worker.