The Inflation of 2021 Through Mid-2022 Is Back, Baby!: Chart of the Day

The return of early-2021 to mid-2022 class inflation: oil shock, sticky core, rate and a Fed on edge as the inflation scare just got real again…

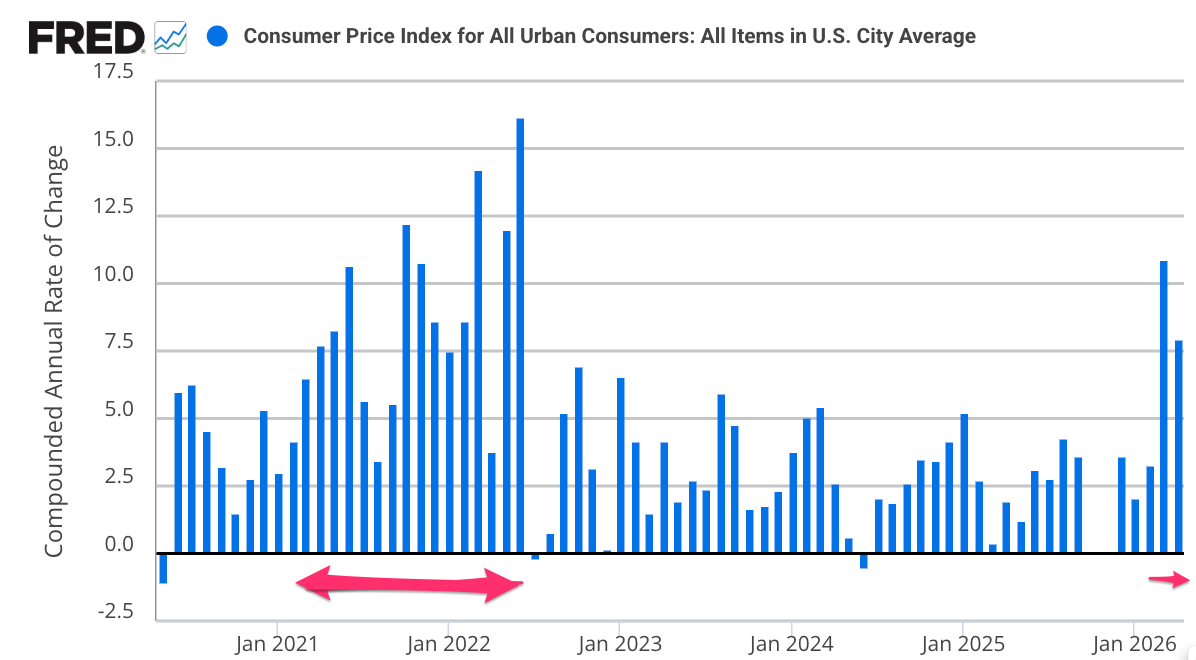

As one of my correspondents says: “The technical term is ‘yuck’…. So much winning…”: definitely renewed “moderate” inflation as a phenomenon, and not just noisy data.

Core inflation (removing food and energy) up at a 4.8% per year rate April/March. Total Consumer Price Inflation up at a 7.2% per year rate. And housing up at at a 7.2% per year rate as well! That is to say: it is not just a volatile-commodities plus, as Treasury Secretary Scott Bessent likes to call it, Straits-of-Vermouth story. This is not consistent with any comforting “disinflation is done, for now” story. That story is dead. Any chance of any even semi-benign glidepath back to 2.5% CPI-basis per year has been rudely interrupted by the rake-stepping of Donald Trump and his corrupt, cowardly minions.

Start with the mechanics. We see a headline reading that is being yanked up by energy: energy prices rose 3.8% month‑over‑month and 17.9% year‑over‑year, with gasoline up a truly eye‑catching 28.4% over the past twelve months. (If you want to teach undergraduates what a relative‑price shock looks like when it hits a consumer price index, you could do much worse than this episode.) This is straight out of the 1970s oil‑shock playbook. But the right way to think about this is not, at least at first pass, as a generalized nominal overheating phenomenon. It is a relative‑price disturbance—oil and energy getting more expensive because of geopolitics, with all the usual knock‑on effects on shipping, risk premia, and supply chains.

Historically, such oil shocks raise measured inflation for a while as energy and energy‑intensive goods become more expensive. Second, they act like a tax on non-oil patch domestic consumers and firms, squeezing real incomes and profit margins, and thereby tending to slow demand. The central question for monetary policy is always: how much of the first effect do you accommodate, and how much do you lean against, given that the second effect is already contractionary? Against that background, what is a sensible Federal Reserve reaction? I think the reasonable stance looks like this:

First, you say: stay on hold longer. Whatever (already very weak) case there was for near‑term cuts premised on steady disinflation toward target is gone, after two months of hot headline and uncomfortable core. You do not cut to validate financial markets’ desire for lower yields when the incoming information set is moving against you.

Second, you say: “higher for longer” louder and more often. That becomes the core of your rhetoric—signal that the modal path for rates now involves policy staying at or near current levels well into 2027, and that the distribution of possible paths is no longer weighted toward cuts.

Third, you do not, if you are sensible, panic: do not hike in response to a relative‑price shock—but you do try to anchor expectations, so that firms and workers do not infer that the central bank will simply look through any and all price spikes. and thereby treat this as a green light for broader cost‑push behavior.

Fourth: staff memos and models start plotting open a future hiking path starting in late 2026, with perhaps some consideration of front-loading before Labor Day to avoid a bigger political mess, given how unhinged not just Donald Trump but the entire White House is.

Fifth, try not to advertise this loudly now: one does not want to manufacture an expectations shock when the underlying driver is geopolitical and, one hopes (increasingly in vain), temporary. But you also do not rule out the possibility that an energy‑driven spike, sustained and amplified by wage‑price feedbacks, will require tightening soon down the road.

Sixth, remember this always: once expectations unanchor, the cost of re‑anchoring is very high indeed.

Seventh, remember that a central bank cannot, by raising short‑term interest rates, produce more Iranian crude or stabilize shipping lanes. It can, however, take an already contractionary real income shock and turn it into a full‑blown recession.

How does this compare with 2021 to mimd-2022?

Back then, we had what in retrospect looks like a remarkably broad and messy inflationary process. There was fiscal stimulus not offset by a central bank that still had valid fears of a return to the ZLB, and wanted to avoid making that a live possibility. There were snarled supply chains, particularly in semiconductors and durable goods. There was housing, with rents and shelter costs rising rapidly as pandemic migration, low rates, and underbuilding interacted. Then Putin’s attack on Ukraine was layered on top, further destabilizing energy and food. Multiple overlapping shocks hitting an economy that had already absorbed a huge fiscal and monetary jolt that, in retrospect, still looks economically-technocratically appropriate to me: rapid return to full employment is a very good and valuable thing to buy at the cost of a year and a half of a very moderate inflation.

However, today’s episode is, so far, narrower and more geopolitically centered. We have a war‑driven oil spike as the only primary driver. Tariff‑related pressures and housing‑sector stickiness are there, but secondary. That matters for how worried we should be about an inflation process that runs away from us.

It also matters where we started. Core inflation on a CPI basis was not that far from what the de facto Federal Reserve target of around 2.5% per year. We were reasonably close to the neighborhood we wanted to live in, even if we had not quite moved into the house and unpacked the furniture.

The risk now is that the combination of an oil‑price shock and a still‑tight labor market nudges that core rate up and keeps it there: as firms look at higher input costs and decide to protect margins; as workers, observing the new headline numbers, push more aggressively for cost‑of‑living increases. If that happens, the story becomes “shift in the implicit inflation norm back toward above 3%”.

Is the right interpretation that disinflation has been interrupted rather than reversed? Maybe. That means: stay the course, extend the horizon for “higher for longer”, talk tougher, and keep a wary eye on core. But do not slam on the brakes just because Donald Trump, stupidly and bloodily, issued an engraved invitation for oil, once again, to join the inflation party.