Theories of Economic History VI: Modern Economic Growth :: Roughly-Edited Transcript:

J. Bradford DeLong brad.delong@gmail.com :: 2026-04-28 :: All Souls’ College, Oxford :: The 2026 Sir John Hicks Memorial Lecture in Economic History…

Link to Video:

<https://braddelong.substack.com/p/theories-of-economic-history-zoom>

And let me start going through, making the transcript less incoherent, less cryptic and compressed, and more sensible…

In 1875, we really did yet again—just as in the exit from the agrarian to the commercial‑imperial age, and just as in the exit from the commercial‑imperial age to the first industrial‑revolution century—get something genuinely new. The world economy, or at least the North Atlantic chunk of it, stepped onto what Simon Kuznets would, much later, label the path of “modern economic growth,” and what Robert Gordon has usefully described as the “one big wave” of transformative technologies between roughly 1870 and 1970. Before that point, even in the relatively dynamic early 19th century, you were talking about perhaps 0.5–1.0 percent per year growth in output per worker in the core. Afterward, in the United States and Germany in particular, trend labor‑productivity growth around 1.8–2.0 percent per year becomes thinkable, and then normal. Doubling times fall from a century to 35 years.

By 1870, the United States had already caught and then overtaken Britain in GDP per capita when measured carefully, at least according to Angus Maddison’s reconstructions and subsequent refinements by people like Stephen Broadberry and co‑authors. Germany, still politically fragmented until 1871 but increasingly integrated economically through the Zollverein, was not far behind. Between 1870 and 1913, U.S. real GDP per capita roughly doubled; German real GDP per capita did something similar; and aggregate output in each case increased by a factor of three to four as populations also grew rapidly. Kuznets, looking at these numbers in the 1950s and 1960s, saw a clear structural break: sustained, compounding growth in output per head, not just in total output, had become the normal expectation rather than the rare exception.

Both the U.S. North and Germany, in other words, did largely independently make this particular jump into what Kuznets called modern economic growth, and into what Gordon calls the “Second Industrial Revolution” wave: electricity, the internal combustion engine, petroleum, chemicals, telephones, reinforced concrete, and the rest of the familiar catalog. Gordon likes to emphasize that, between 1870 and 1970, this wave drove U.S. real output per capita up by something like a factor of seven, and transformed everyday life far more radically than the digital technologies of the late 20th and early 21st centuries have yet managed. Indoor plumbing alone probably did more for human welfare than a thousand smartphone apps.

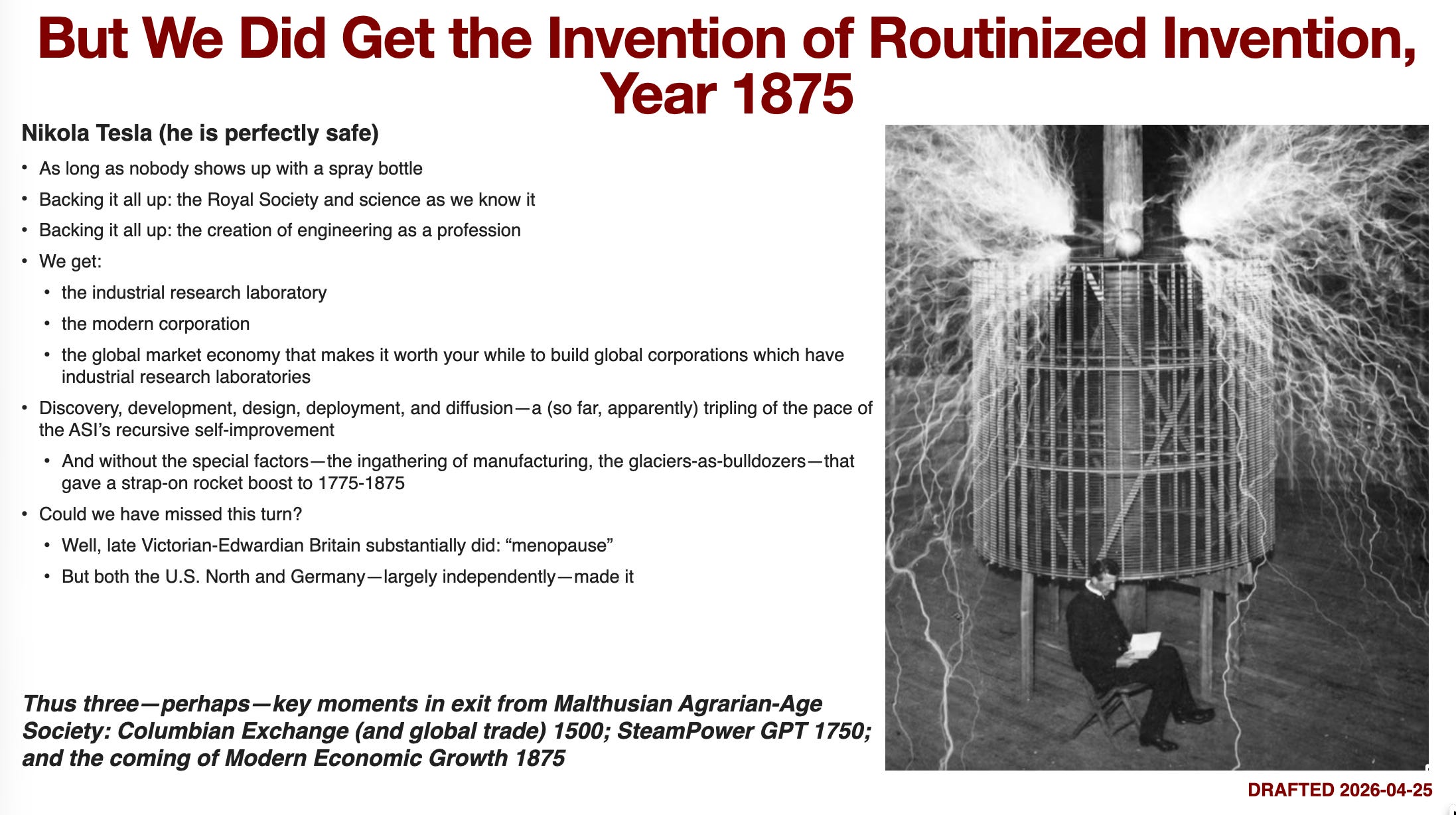

What, then, was new? We got what I call the invention of routinized invention. It is not that human beings had not been inventing things before; it is that around 1875 the social and institutional machinery for turning inquiry into invention, and invention into widely diffused technology, became systematic, large‑scale, and semi‑predictable. I have a picture in my mind of Nikola Tesla demonstrating to journalists and others exactly how weird and crazy and powerful he is, how he seems to control the lightning and is actually perfectly safe—or at least he is perfectly safe if no one comes running in with a spritzer spray bottle, because the low‑humidity air of Colorado is a very good insulator, right? And decaying exponentials decay very, very fast. Also, it is a trick of the camera: the closest discharge is 30 feet away from him. It is theater as much as physics.

It is, nonetheless, an impressive advertisement for why you should hire Tesla as your chief engineer. I agree, and he was a very impressive guy: by 1896 he was designing polyphase AC systems that made it possible to transmit electricity tens and then hundreds of miles, and by the time the Niagara Falls power project came online, you had a practical system that turned falling water into cheap power for factories, streetcars, and homes over a wide radius. That was not marginal; it cut effective energy costs for some kinds of use by an order of magnitude and, as economic historians of technology like Paul David have noted, it enabled the reorganization of factories from vertical‑shaft, line‑shaft layouts to flexible, electric‑motor‑at‑each‑machine layouts. That reorganization alone generated perhaps 30–50 percent productivity gains over several decades, once firms learned how to reengineer workflows around electricity.

But it is not just a stray genius from Croatia who, although he did know how to make alternating‑current electrons get up and dance in a way that no one else did at the time—genuinely no one else did, and many did not believe it was possible at all. If the 19th century were just a story of isolated prodigies—Tesla, Edison, Siemens, Daimler, Diesel—then we would not see the broad, sustained, cross‑sectoral acceleration that people like Gordon, Crafts, and Mokyr document. The key is that by 1875 those geniuses were embedded in, and backed by, a new infrastructural complex: scientific societies, engineering schools, corporate R&D labs, patent systems with reasonably well‑defined rules, and capital markets capable of financing very large, very long‑horizon projects.

You have to have them backed up by the Royal Society and science as we know it, with their empirical orientation—that peculiar cultural shift toward “nullius in verba,” toward the idea that experiment, measurement, and mathematical modeling trump tradition and authority. You have to back it all up with the creation of engineering as a profession: not a handful of inspired tinkerers, but, by 1900, tens of thousands of trained engineers in the United States and Germany alone, graduating each year from places like the Massachusetts Institute of Technology (founded 1861), the Technische Hochschulen in Berlin and Munich, and land‑grant universities across the American Midwest. By the eve of World War I, the U.S. was minting perhaps 5,000 engineering graduates a year—a small number by today’s standards, but orders of magnitude beyond anything the early 19th century had seen.

Why did that matter? Because steam engines, and then turbines, dynamos, chemical plants, and railways broke all the time. They were complex, high‑pressure, high‑voltage, high‑temperature systems. To keep them from exploding, melting down, or simply grinding to a halt every few weeks, you needed a stratum of people who not only could turn a wrench but also could read a diagram, do some thermodynamics, think in terms of stress tolerances and failure modes. Nathan Rosenberg, among others, has stressed that much of “technological progress” in this era was actually incremental improvement and learning‑by‑doing in operation and maintenance, not just the initial stroke of invention. That kind of incremental improvement requires routinized human capital.

And with that bundle of institutions and human capital, we got the modern industrial research laboratory: Edison’s Menlo Park in the 1870s and 1880s; the establishment of corporate research labs at General Electric, Westinghouse, Siemens, and AEG in the 1890s and early 1900s; the rise of the German dye and chemical industry’s laboratories (BASF, Bayer, Hoechst), which by 1913 had made Germany the world’s dominant producer of synthetic dyes and a leader in industrial chemistry. By the 1920s and 1930s, you see Bell Labs in the United States adding telecommunications and materials science to the mix. Joel Mokyr likes to talk about the “Industrial Enlightenment,” in which formal scientific knowledge and practical tinkering fuse and feed back into each other; the late 19th‑century research lab is where that fusion becomes bureaucratically embedded.

We also got the modern corporation: multidivisional, professionally managed firms with the ability to mobilize vast amounts of capital and to coordinate production at continental scale. Alfred Chandler’s “visible hand” analysis of firms like Standard Oil, U.S. Steel, and DuPont underlines how organizational innovation—integrated supply chains, internal capital markets, salaried management hierarchies—was as important as any individual technology. By 1910, the largest U.S. corporations had workforces in the tens or hundreds of thousands and capitalizations in the hundreds of millions of dollars, something like 1–2 percent of U.S. GDP for a single firm. That scale mattered, because it made it worthwhile to fund in‑house laboratories, to run large‑scale experiments, and to roll out new technologies across entire industries.

And we got the global market economy that makes it worth your while to discover, develop, deploy, and then for others to diffuse the technologies of nature manipulation and also of human organization that have made us now so rich. Between 1870 and 1913, global trade as a share of world GDP roughly doubled; world exports rose from perhaps 5–6 percent to over 12 percent of world output. Capital flows surged: British foreign assets, for example, climbed from about 7 percent of British wealth in 1870 to nearly 50 percent by 1913, as London financed railways in Argentina, mines in South Africa, and utilities in the United States. Kevin O’Rourke and Jeffrey Williamson quantify the resulting price convergence in commodities, wages, and interest rates and argue that this first age of globalization created both enormous opportunities for technology diffusion and enormous distributional stress.

Could we have missed this turn to the modern economic‑growth world of the research lab and the corporation? That is not a silly question. Late Victorian and Edwardian Britain appears to have substantially missed, or at least fumbled, it, in spite of having had the best scientists—back in the day when James Clerk Maxwell was, as contemporaries half‑joked, the only person who really understood electromagnetism at a deep theoretical level. Britain led in pure science and in the first industrial revolution’s technologies: steam, cotton, iron. Yet, as economic historians like David Edgerton, Martin Wiener, and more Chandler‑inflected analysts have complained, Britain did not invest as heavily or as effectively in the second wave’s corporate structures and engineering‑intensive industries: electrical machinery, chemicals, automobiles.

Earlier economic historians worried over this problem and gave it the very strange name of “Britain’s menopause,” which tells us interesting things about their general orientation and their comfort with gendered metaphors that have not aged well. The underlying question, however, remains live: why did Britain’s relative productivity performance sag after 1870, especially in manufacturing sectors where the new capital‑ and R&D‑intensive technologies mattered most? Crafts and Toniolo, in their work on European “catch‑up and convergence,” and Broadberry and colleagues, in their sectoral reconstructions, show Britain moving from unambiguous leader in 1870 to a country being caught and overtaken by the United States and Germany in many key industries by 1913. The puzzle is that Britain had many of the prerequisites—capital, scientific prowess, empire—yet stumbled in the institutional shift to routinized invention inside large firms.

On the other hand, both the U.S. North and Germany largely independently did make this particular jump into what Kuznets called modern economic growth. The U.S. North did so off the back of a huge internal market, a relatively high‑wage labor force, and abundant natural resources; Robert Allen has argued that this “high wage, resource rich” environment made capital‑intensive, energy‑using technologies especially profitable there. Germany did so with a different model: strong technical education, close collaboration between universities and industry, and a banking system (the universal banks) willing to take long‑term positions in industrial firms. In both cases, however, the pattern is the same: you see the institutionalization of invention—labs, engineering corps, corporate hierarchies—combined with access to large markets and supportive states. The result is that by 1913, the United States and Germany have not only joined the club of rich nations but have helped redefine what “rich” means: not a static rent‑extraction equilibrium, but a world in which 1.5–2.0 percent annual growth in productivity is built into the bones of the system. That is the structural shift that “1875” symbolizes.

Both the U.S. North and Germany largely independently did make this particular jump into what Simon Kuznets called modern economic growth, and what Robert Gordon calls the one big wave since 1875.

Well, now, today we have on the order of 8.4 billion people alive on the planet, rather than the perhaps 1.3 billion of 1875. Back then, something like one person in six on earth lived in Europe, perhaps one in ten in the Americas, and the rest in Asia and Africa; now we have a world in which the population share of Europe has fallen below 10%, East and South Asia together account for well over half of humanity, and Africa’s share is rising rapidly toward one quarter. If you take world GDP today as something like 150 trillion dollars a year in purchasing‑power‑parity terms, and divide by those 8.4 billion people, you get on the order of 18,000 dollars per capita per year—extraordinarily unequally distributed, of course, with rich countries at 50,000–80,000 dollars per head and the poorest still stuck at 2,000–3,000. But even that 18,000 dollar average is roughly six times the perhaps 3,000 dollars (in today’s prices) that the average person in 1875 might have had to scrape by on.

Over 150 years, to go from 3,000 to 18,000 dollars per capita is a factor of 6; the compound‑annual‑growth‑rate arithmetic gives you about 2.02% per year. That is more than three times the global pace of technological advance and productivity growth during the “classic” Industrial Revolution century from, say, 1770 to 1870, when the world as a whole might have managed 0.6% per year at best. And it is easily 10 times—or, if you take the more pessimistic view of pre‑1500 growth rates, perhaps 50 times—the pace of the agrarian age, when 0.02–0.05% annual growth in output per capita is the sort of number economic historians like Gregory Clark or Oded Galor throw around.

Put differently: if your world is growing at 0.03% per year, it takes more than two millennia to double average living standards. At 0.6% per year, as in the early industrial centuries, doubling comes every 85 years or so. At 2.00% per year, you double in roughly 35 years. You can see why, as Robert Gordon keeps insisting, the past century and a half looks like a “one big wave” anomaly when set against the exceedingly flat line of the preceding six or eight thousand years.

From that perspective, the cliché about “more technological change in two years now than the medieval world would have seen in a century” is not just rhetorical inflation. Take the High Middle Ages, 1000–1300: you do get some important innovations—heavy plow, horse collar, water mills, windmills, three‑field system, some modest improvements in ship design and accounting—but they diffuse slowly, over generations, and often with maddening lags between technical possibility and widespread use. Measured in terms of productivity growth, careful reconstructions suggest Europe might have managed perhaps 0.1% per year in a few especially dynamic centuries. By contrast, in the United States in the 20th century, Robert Gordon calculates average labor‑productivity growth at roughly 2% per year, and in the extraordinary quarter‑century from 1920 to 1945 something closer to 2.5–3%. On that metric, a single decade in a mid‑20th‑century industrial core country is, in terms of efficiency gains and new capabilities, the rough equivalent of several medieval centuries.

And so these now become the overwhelming facts of human economic history. The big story is no longer “why are we so poor?,” which was the relevant question from Uruk through Louis XIV, but “how did we get so rich so fast, and why is it so unevenly shared, and what damage are we doing to the biosphere as we go?” That is the axis along which the work of people like Kuznets, Maddison, Pomeranz, Allen, Mokyr, Gordon, and Deaton lines up.

For one thing, the demographic transition becomes inescapable under these conditions. All paths that would keep us in a Malthusian world vanish. If you can reliably earn enough over your lifetime to support yourself and perhaps a small household without needing six surviving children as a form of old‑age insurance, and if you have means of artificial birth control that are cheap and reasonably accessible, and if you are not desperate to have a surviving son to inherit the family plot because your life chances do not depend on that plot, then, all across the world, revealed preference appears to be that rather more women (and men) would prefer to have one or two children than three or four.

The numbers tell that story. In 1875, global fertility rates were likely in the range of 5–7 births per woman almost everywhere outside a handful of already‑urbanizing pockets. Today, world total fertility is below 2.4 births per woman, and falling. In East Asia and much of Europe, it is well below replacement, at 1.2–1.6. Even in countries that were at 6–7 births per woman in 1960—say, Mexico, Brazil, South Korea, or Iran—fertility has fallen below or near replacement in a single human lifetime. The demographers’ maps show a cascade spreading from the North Atlantic outward: France’s fertility decline in the late 18th century, Britain’s and Scandinavia’s in the 19th, Southern and Eastern Europe’s in the early 20th, the Americas’ and East Asia’s in the late 20th, and now, increasingly, parts of South Asia and Africa following. That pattern is what made Oded Galor and his colleagues confident enough to try to wrap the whole process in a “unified growth theory”: a once‑and‑for‑all takeoff in productivity induces a once‑and‑for‑all stabilization and then decline in fertility.

And this 2% per year we have been casually throwing around is measured on what might be called a “necessities‑and‑conveniences” basis. It is mostly about stuff you can count in national accounts: tons of steel, kilowatt‑hours, hours of schooling, years of life, cars, refrigerators, square feet of housing. This does not take account of all the Dixit–Nordhaus–Trefler considerations, and their intellectual cousins, about the value of increased lifespan, the value of an increased variety of commodities, and the consumer surplus embedded in things that are priced at or near zero.

Take lifespan. In 1875, average life expectancy at birth globally was perhaps 30–35 years. In the richer parts of Western Europe, you might have seen 40–45; in China or India, maybe 25–30. Now the global figure is near 73; in rich countries, 80 and above. A doubling of life expectancy is, in some sense, at least as important as an equivalent proportional gain in annual income. William Nordhaus once tried to value this shift and concluded that the gains from increased longevity in the 20th century alone were on the same order of magnitude as the measured gains in consumption. That is, our GDP numbers are missing roughly half the real improvement.

Then consider variety. In 1875, the average household in even a rich country might have access to a few dozen distinct categories of goods and services: perhaps a handful of staple foods, a few textiles, simple tools, limited entertainment. Today, a supermarket carries tens of thousands of SKUs; the app store on your phone has millions of offerings; the global supply chain pours an essentially unbounded variety of differentiated products into even middle‑income cities. Avinash Dixit and Joseph Stiglitz built a whole branch of trade and industrial‑organization theory out of the idea that people value variety in and of itself, and that more differentiated product space is a welfare gain even if aggregate “quantity” is unchanged. Paul Romer took that intuition and put it at the heart of his endogenous‑growth story: new ideas translate into more distinct intermediate goods, which in turn increase productivity.

And then there is the fact that, for many of the things that loom so large in our utility functions, market prices are either zero or badly misleading. Think of search engines, digital maps, Wikipedia, open‑source software, free messaging, streamed media at near‑zero marginal cost. The national accounts record a few hundred billion dollars a year for the revenues of tech platforms; they do not and cannot record the trillions in consumer surplus. It is here that people like Hal Varian step forward to say: if you tried to adjust for these things properly—longevity, variety, quality improvements, new goods, unpriced digital services—the true underlying rate of economic growth, in welfare terms, is probably much, much bigger than the 2.65% per year that shows up in the GDP tables. Nordhaus’s “price of light” thought experiment—which traces how many hours of work it took to buy an hour of illumination from candles, oil lamps, gas lamps, and electric bulbs—suggests welfare gains of factors of 100 or 1,000 that standard price indices miss. Varian’s back‑of‑the‑envelope numbers for the value of search or maps carry a similar flavor.

And yet, subjectively, many of us feel pretty close to satiated in at least some domains. God knows I do not want any more sweet wheat‑based pastries in my life; the marginal cronut provides sharply diminishing returns. I emphatically do not want any more emails in my life, given how I keep feeling I have to keep up with more and more digital chatter in order to even do my day job and be amused. At the extensive margin, I am pretty satiated with a great many goods: I do not particularly need a fourth screen, a fifth pair of shoes, or a larger refrigerator. And yet I, and I think many others in high‑income societies, still look forward to new discoveries, to new goods, to new capabilities. We hunger, very much, for variety, for quality, for time‑saving, for reductions in hassle and friction rather than for raw tonnage of stuff.

Those dimensions—variety, quality, freedom from drudgery, access to information and connection—have to go into any proper wealth accounting. If you try to write down a social‑welfare function that accounts for them, and then ask “at what rate is this welfare function growing?”, you will get something that, as Varian and other digital‑economy optimists would suggest, is probably substantially larger than 2.65% per year, at least in the parts of the world where the information‑and‑services economy is fully present. Angus Deaton’s work on consumption, health, and wellbeing pushes in the same direction: the story of the past 150 years is not just about more calories and more square feet, but about radically lower infant mortality, vastly reduced pain and risk in childbirth, and the near‑vanishing of famine outside war zones.

You know, that really matters. By now we are not just talking about a modest uptick in the rate at which we add incremental gadgets to our lives. We are talking about an extraordinary, orders‑of‑magnitude improvement in the human ASI’s ability to recursively self‑improve itself—that is, the ability of the global collective intelligence embodied in scientists, engineers, organizations, and institutions to generate new ideas that make it easier to generate yet more ideas. Joel Mokyr’s “cloth of knowledge” metaphor, Elhanan Helpman’s models of idea‑driven growth, Paul Romer’s famous line about “non‑rivalry” and “ideas having increasing returns”: all of those are attempts to get at the same thing. Once you have a system that can, on its own, sustain 2.65% annual improvement in average material living standards for a century and a half, you have created something that no pharaoh, no emperor, no medieval king, and indeed no 18th‑century philosophe would have recognized: an economy whose default state is exponential, not static, and whose main problems are no longer scarcity in the old Malthusian sense but distribution, stability, and the ecological and political consequences of its own runaway success.

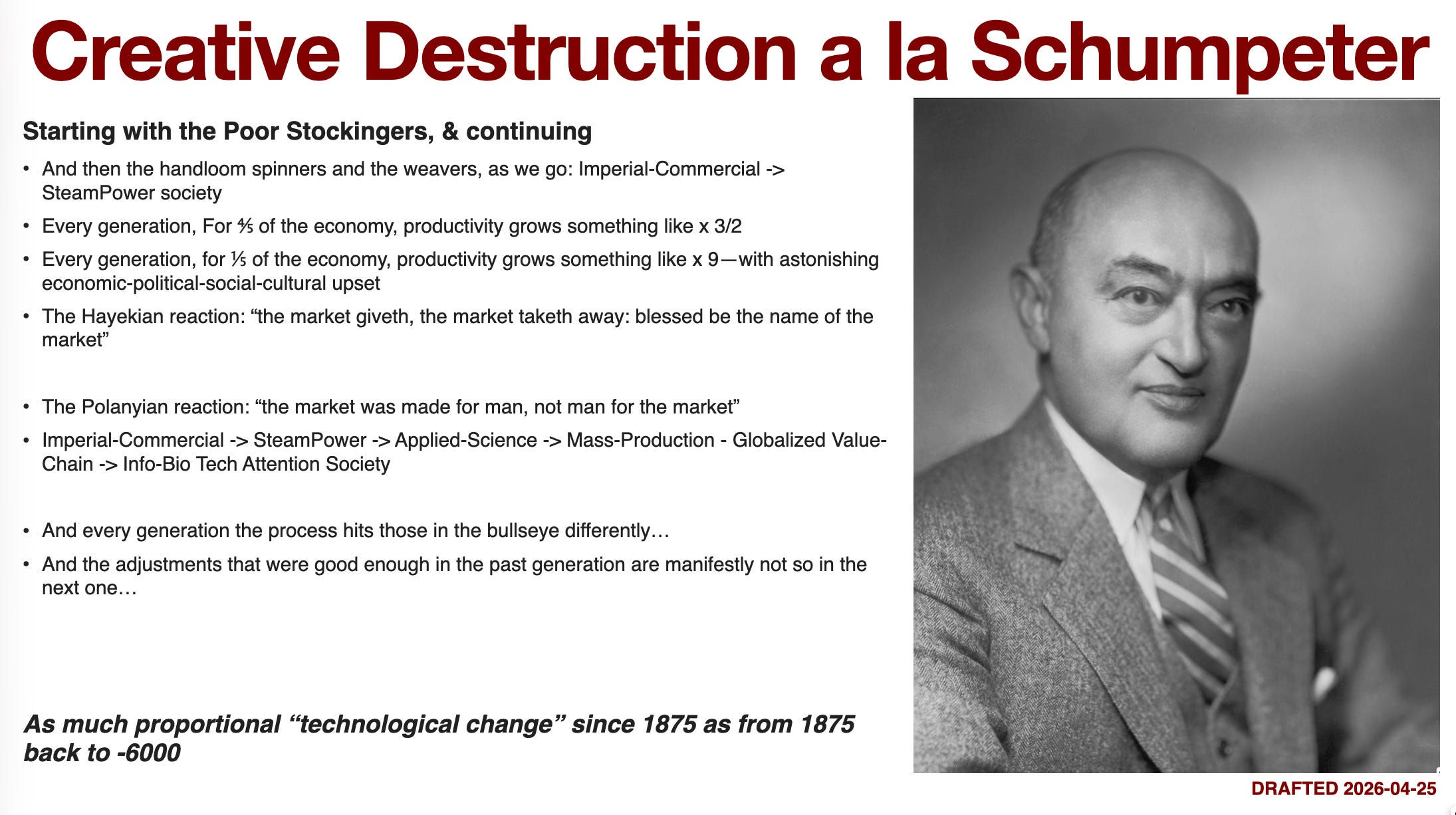

And we also have to start talking about Joseph Schumpeter.

Take that roughly 2% per year growth in labor productivity that has characterized the industrial core since, say, 1870: a 35‑year doubling time, a tripling of our technological capability to produce necessities and simple conveniences every 45 years or so. If you start with an index of 100 in 1870, then by 1910 you are near 200; by 1955 you are around 400; by the end of the 20th century you are well above 800. Robert Gordon calculates that between 1870 and 1970 U.S. output per hour rose by a factor of about 8, while Angus Maddison’s reconstructions tell a similar story for the broader North Atlantic. That is the arithmetic behind what Schumpeter called “creative destruction”: not a gentle rising tide but a storm surge that keeps ripping up and rebuilding the shoreline.

But Schumpeter’s point, and I think he is right here, is that this 2% is not evenly distributed across sectors or across cohorts. For every generation, say for 4/5 of the economy, there is productivity improvement of something like 50% over 40 years or so. If you are in haircuts, restaurant meals, primary schooling, nursing, or live performance, you see better tools, better organization, a somewhat more educated workforce, but the basic production function does not change that much. William Baumol warned us long ago that these “stagnant” sectors would see rising relative costs precisely because they do not enjoy transformative productivity growth.

But for 1/5 of the economy, in each generation, productivity improves by something like a factor of 9. In Gordon’s “big wave,” those sectors were electricity, internal combustion, chemicals, telephony, steel, then later aviation, household appliances, and the modern factory. A nine‑fold improvement over 40 years is on the order of 5–6% annual productivity growth. That is enough not just to shift relative prices but to destroy and recreate entire ways of life. In 1900, perhaps 40% of the U.S. labor force worked in agriculture; by 2000, that was under 2%. In 1950, manufacturing was roughly one‑third of U.S. employment; now it is under 10%. The workers did not all vanish; the tasks did.

Consider some concrete cases. In 1910, the United States had on the order of one million telephone operators, the vast majority of them women, physically plugging cables into switchboards to connect calls. They were high‑tech workers by the standards of the day. By the 1970s, electronic switching had eliminated almost all of these jobs. The occupation effectively went from “mass female employment gateway into the middle class” to “historical curiosity” in a single lifetime. Economic historians of technology such as Claudia Goldin and James Bessen have documented how the diffusion of automatic switching first raised demand for operators and then, once the technology matured, drove it toward zero.

Or take the legions of back‑office workers adding up and checking columns of numbers—the bookkeepers, human “computers,” and clerks who were, in Alfred Chandler’s phrase, the “visible hand” of the large corporation. In 1900, a serious insurance company, railroad, or bank employed entire floors of people doing double‑entry bookkeeping by hand. Irving Fisher, writing The Rate of Interest in 1907, thanks his “computer” at Yale—a woman sitting with a mechanical calculator—for grinding through the numerical examples. At Los Alamos in the 1940s, Richard Feynman and his colleagues described how they devised the equations and algorithms while some 40 women with desk‑sized calculators did the actual number‑crunching to see whether the bomb design would work. By the 1970s, mainframes and then minicomputers had made that entire mode of clerical work obsolete.

We can put some rough numbers on this banishing of sectors. In 1950, clerical and administrative support jobs were roughly 18–20% of U.S. employment; by 2020 that share had fallen by about a third, even as the volume of information processed exploded. Agriculture dropped from about 11% of employment in 1950 to under 2% today. Routine production jobs—assembly‑line work in auto plants, steel mills, appliance factories—peaked in the 1960s and 1970s and have shrunk sharply since, due both to automation and to trade. David Autor, David Dorn, and Gordon Hanson have painstakingly charted how routine, codifiable tasks are precisely those eaten first by computers and robots.

The banishing of entire sectors, then, goes hand in hand with the creation of enormous opportunity if you are riding the wave of the GPT sectors—general‑purpose technologies like electrification, information technology, and now machine learning. If you happened to major in electrical engineering in 1920, computer science in 1980, or data science in 2010, you were in the updraft. If your skills, location, and social capital matched the needs of the expanding 1/5 of the economy, your real earnings could double or triple over a career, and you could plausibly imagine your children doing even better.

But there is also rapid, rapid impoverishment and life destruction if you are not. For the displaced operator, bookkeeper, assembly‑line worker, or smallholder farmer, the local labor market does not automatically conjure a new high‑productivity sector nearby. Barry Eichengreen and others have talked about the “Great Compression” in mid‑20th‑century America, when institutional arrangements—unions, wage norms, progressive taxation—kept distribution relatively equal even as the pie grew. Since the 1980s, those arrangements have weakened: in the United States, the labor share of income has fallen a few percentage points, union density has collapsed from over 30% to under 10%, and the top 1% have gone from capturing perhaps 8% of income to over 20%. The dislocation costs of creative destruction now land on less cushioned backs.

All this takes place in the context of a political‑economic world that is, I think, fundamentally split between two moral‑intellectual allegiances. On one side is the camp that lines up behind something like Friedrich von Hayek’s decree: the market can produce prosperity, and we dare not ask it to do anything more. Our role, in this view, is to maintain the rule of law, protect property rights, and then humbly accept the pattern of rewards and punishments that decentralized market processes generate. As in the Book of Job, the market giveth, the market taketh away, blessed be its name. Attempts to temper or redirect its judgments, in this reading, will bring only inefficiency and, eventually, tyranny.

On the other side is the camp that lines up behind something like Karl Polanyi’s retort: wait a minute, the market is made for man, not man for the market. A self‑regulating market in labor, land, and money is not a natural order but a political construction, and it will, left unchecked, tear apart the social fabric that makes human life bearable. Polanyi’s The Great Transformation is, among other things, a history of how 19th‑century Britain’s experiment with laissez‑faire generated such intense social dislocation that it called forth a double movement: protective legislation, social insurance, and political mobilization to blunt the market’s sharpest edges. To treat the wage share, the unemployment rate, or the income distribution as morally untouchable outputs of an infallible algorithm is, for this camp, an abdication of democratic responsibility.

In every generation, different people are in the bullseye, different kinds of people are in the bullseye. The British handloom weaver of the 1820s, undercut by power looms in Lancashire, is not the same as the Detroit autoworker of the 1980s, squeezed by Japanese competition and industrial robots, or the radiology technician of the 2030s, staring at an AI system that reads scans more accurately than any human. Yet each, in their moment, occupies the intersection point where Schumpeterian innovation slams into the real lives of ordinary households.

And in every generation, the adjustments that seemed to produce a tolerable, at least political‑economic order in the previous generations somehow seem to fail, and fail. The 19th‑century answer—charity, poor laws, emigration—crumbled under the strain of mass urbanization and industrial labor. The mid‑20th‑century answer—strong unions, bounded finance, welfare states, Bretton Woods capital controls—has been eroded by globalization, technological changes in production, and ideological shifts toward deregulation and “shareholder value.” Economic historians like Peter Lindert and Jeffrey Williamson have tried to measure the long‑run arc of inequality and redistribution; their numbers tell a story of recurring cycles in which institutions briefly catch up to the pace of change, only to be outrun again.

That, I think, is the Schumpeterian world we inhabit: not a smooth 2% glide path, but a succession of sectoral earthquakes, with each cohort of winners and losers forced to renegotiate its relationship to the market, the state, and the social contract—over and over, at an accelerating tempo, with no final settlement in sight.

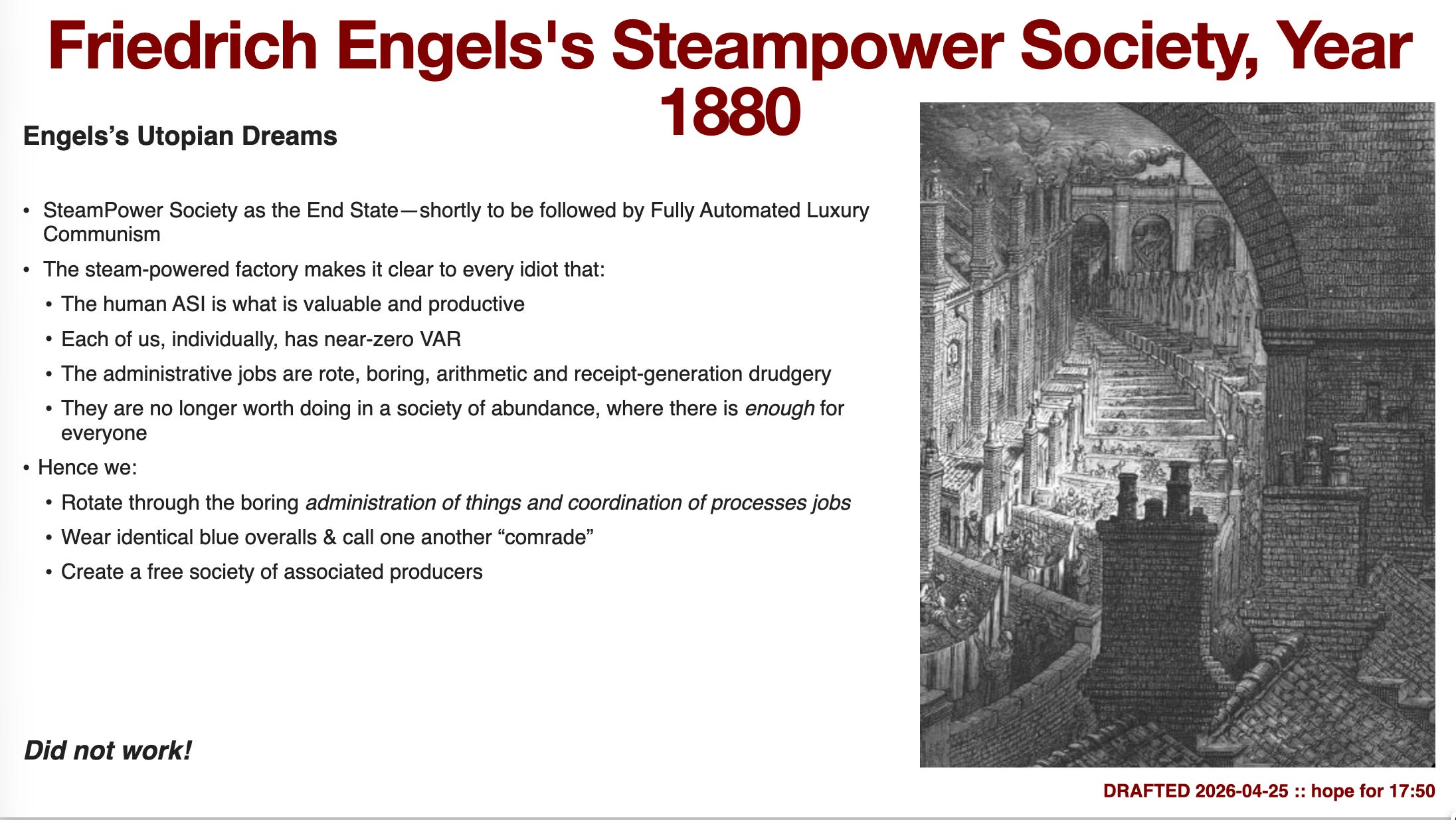

Friedrich Engels thought there was going to be a settlement—and that it was obvious that it would be a very good settlement. A beneficial and benevolent end of history.

Engels looked at the steam‑power society of the late nineteenth century and took it, more or less, to be the revealed “final form” of industrial technology. Around 1870 there were perhaps 30–35 million people in Britain and 400–450 million in Europe as a whole; something like 40–45% of the British labor force was still in agriculture, but in the industrial districts the factory had become the dominant life-world. Steam engines in Britain alone were delivering mechanical power equivalent to tens of millions of human laborers. By 1900, British coal output had reached roughly 225 million tons a year, and perhaps half of all mechanical work in the country was being done not by human or animal muscle, nor by water, but by steam. To Engels, gazing out from Manchester and London, it looked as if the logic of the system was already fully on display.

You had big, lumpy steam engines that were expensive, indivisible, and had to be used at scale. A Watt or Corliss engine was a fixed-cost monster: capital tied up in a single machine that had to run as close to 24/7 as possible to earn its keep. That meant you gathered hundreds or thousands of workers into large factories to make use of that big fixed‑capital machine. In 1861, the average textile mill in Lancashire might have a few hundred workers and one or two huge engines; by 1900, the big urban plants in Britain, Germany, and the U.S. North routinely employed thousands. From inside that world, it seemed blindingly clear that what was truly valuable and productive was the collective “human ASI”—the whole web of human brains in cooperative production—while each of us, taken individually, had only a small marginal value above replacement. One spinner or weaver more or less did not matter; the fact that there were 2,000 of them, synchronized with the engine and the looms, very much did.

In Engels’s reading, the hierarchy that survived from the agrarian age had already lost most of its justification. Administrative jobs in the steam age were, in his mind, mostly rote: boring, repetitive work—bookkeeping, tallying, checking receipts, pushing paper—rather than any kind of deep, irreplaceable statesmanship. The clerk with the quill and the ledger in a railway office, the overseer with a stopwatch on the factory floor, the gentleman at a City bank shuffling bills of exchange: none of these, in Engels’s eyes, were doing anything that required a life‑time claim on authority and surplus. The boss’s role was not that of a wise coordinator of dispersed, tacit knowledge but of a rent‑extractor perched atop an increasingly self‑running machine.

And once society was rich enough—once steam and machinery had delivered material abundance at scale—why would anyone still accept “being the boss” as a morally or psychologically attractive role? By 1870, British GDP per capita was perhaps 3,500–4,000 dollars a year in today’s prices, a multiple of what most humans anywhere had ever seen. Even in the industrial slums, Engels could see that average caloric intake, clothing quality, and access to cheap manufactured goods had risen dramatically relative to 1750. If you projected that trajectory forward a little—another doubling or two—it was easy, perhaps too easy, to imagine a world in which scarcity had been largely banished and the moral foundations of hierarchy simply evaporated.

Engels thus expected the steam age to make class hierarchy not just unjust, but stupid. In a society of abundance, nobody would need to be part of a gang, doing unpleasant, risky, dangerous, boring jobs, simply to have enough to eat and a roof over their head. The miner descending into a pit 500 meters deep in the Ruhr, the dockworker hauling sacks in Hamburg, the match girl in London’s East End: these exist because society is poor and disorganized. Once that material insecurity was gone, he thought, people would no longer tolerate domination. The remaining “administration of things” would be, as he and Marx kept saying, a set of routine coordination tasks that could and should be rotated among everyone.

From this, he projected a very specific utopia. Once you got to a steam‑powered society, Engels said, the logic of production and the moral sentiments of the workers would inevitably push you to a world where:

we all rotate through the boring administration and coordination jobs,

and then spend the rest of our work lives doing something genuinely creative

with our hands and minds.

In his vision, everyone would be a producer and a citizen on roughly equal terms. We would all wear identical blue overalls, call each other “comrade,” and collectively manage the factory and the polity. The “free association of producers” would replace both capitalist firms and class‑stratified states. The 10–15% of national income that, in late‑nineteenth‑century Britain, accrued as rents and profits to the upper classes would be socialized and redeployed; the 1–2% of the population that constituted the traditional elite would be demoted to ordinary comrades. If you read him with some sympathy, you can absolutely see its attraction: stand on the floor of a steam‑powered factory in 1870, look up at the belts and shafts driven from a single engine, and imagine what things will be like once the machine is big enough and efficient enough that scarcity has been banished. You have, in Gary Gerstle’s phrase, a “forging” moment—except Engels thinks the forging will be socialist rather than nationalist or corporatist.

But that is not how history went.

We did not freeze in place at the steam‑power stage that Engels thought he was extrapolating from. Instead, over the late nineteenth and twentieth centuries we moved from a steam‑power society into what we might call an applied‑science society. Electricity, internal combustion, chemicals, telecommunications, electronics, computing, and now digital networks and machine learning—this sequence of general‑purpose technologies reorganized production far beyond the big, loud, coal‑fired factory that was Engels’s archetype. Economic historians of technology like Joel Mokyr and Paul David have spent careers arguing that the Second Industrial Revolution (circa 1870–1914) and the subsequent electrification, internal‑combustion, and information‑technology waves were at least as transformative, and in many ways more so, than the original steam‑cotton‑iron nexus.

Two things followed that cut directly against Engels’s expectations.

First, the role of “administration” did not remain rote and easily rotated. As large corporations, states, and transnational institutions grew more complex, good management became, once again, a highly specialized, high‑rent skill. By 1913, the world now had giant multidivisional firms like U.S. Steel, General Electric, Siemens, and BASF; by 1950, the Fortune 500 was dominated by conglomerates with tens or hundreds of thousands of employees. Alfred Chandler’s history of the modern corporation—“The Visible Hand”—is essentially the story of how a new managerial class re‑legitimized hierarchy by making it productive again. It shows, with numbers and case studies, that firms with better internal information systems, career bureaucracies, and managerial hierarchies actually did produce more output per unit of input than their more ad hoc rivals.

The administrative task set was also no longer simply “count the bales and balance the books.” It was: design R&D programs with hundred‑million‑dollar budgets, coordinate global supply chains, manage regulatory arbitrage across jurisdictions, play three‑dimensional chess in financial markets. The share of managers and professionals in the labor force in rich countries rose from under 10% in 1900 to 30% or more by the end of the twentieth century. That is not something you can rotate through on Tuesday afternoons after your stint at the lathe. The world did not converge on “everyone takes a turn at the boring jobs”; it converged on large, technically sophisticated organizations run by professional elites who could plausibly claim that their skills justified high and persistent rewards.

Second, political democracy did not translate into socialist “end of history” outcomes even where workers had the vote. In the actually existing twentieth century, self‑described “true socialists” in rich democracies rarely commanded more than about 40% of the vote in free, fair elections. In Germany, the Social Democratic Party became the largest party in the Reichstag by 1912, but was still far short of a majority; in Britain, Labour only formed a stable majority government after 1945 and then governed as a party of mixed‑economy social democracy rather than Engelsian abolition of wage labor; in France and Italy, the communist and hard‑left socialist parties that came closest to Engels’s blueprint were kept permanently out of full governing power in the Cold War era. Social democracy and labor movements did win important reforms—welfare states, social insurance, co‑determination in some places, public health, mass education—but Engels’s imagined world of universally associated producers, blue overalls, and comradeship remained a minority taste.

The modal voter in the rich world opted for mixed economies, and not the abolition of capitalist hierarchy—and that was if they did not opt to become the sheep of some ethno‑nationalist kleptocrat‑grifter instead. The interwar period alone—Mussolini in Italy, Hitler in Germany, Franco in Spain, a long list of authoritarians in Eastern Europe and Latin America—should have cured anyone of the belief that giving the franchise to workers automatically yields socialist egalitarianism. Adam Tooze and Barry Eichengreen have both underlined how, when mass democracy confronted economic crisis, the range of outcomes included social democracy, yes, but also fascism, technocratic authoritarianism, and various hybrids.

Quantitatively, the political “left” in most OECD countries since 1945 has oscillated in the 30–45% vote‑share band. In the high point of postwar social democracy—Sweden in the 1960s and 1970s—you got top marginal tax rates near 80%, union density above 70%, and a very compressed wage distribution; even there, however, capitalist firms, managerial hierarchies, and financial markets remained central. In Britain and the United States, postwar social compromise took the form of welfare states and regulated capitalism, not “free associations of producers.” And from the 1980s onward, as Thomas Piketty and his co‑authors have documented, we see a partial reversal: top income shares rising again, wealth concentrating, and what he calls a “Brahmin left” fighting a “merchant right” over an electorate fracturing along education, age, and identity lines rather than a simple capital‑labor cleavage.

So Engels’s steam‑age extrapolation turns out to have been a powerful, enticing misread of what industrial modernity would become. The factory floor he saw in 1870 really did hint at the obsolescence of some old forms of domination: the landed aristocrat and the priest no longer had much to say about how the looms ran; the military‑feudal caste’s skills were not what powered the steam engine. What he did not foresee was that the next wave—the applied‑science society—would generate new scarcities (of cognitive and organizational skills, of political stability, of environmental sinks), new complexities (in finance, regulation, global production networks), and new forms of hierarchy (managerial, technocratic, data‑broker, platform‑owner), and that politics would settle around a much messier, more contested, and far less utopian equilibrium.

Economic historians who look back across the long twentieth century—people who obsess over national accounts from 1870 onwards, and over the details of how firms and states actually work—tend, I think, to share a common judgment here. The great post‑1870 story is not the smooth convergence to a classless society of associated producers, but the emergence of what one might call High Modern Capitalism: a system in which 2–3% annual productivity growth is normal, in which the state is large (30–50% of GDP), in which corporations are powerful and bureaucratic, and in which democracy coexists uneasily with inequality and recurrent crisis.

It is a world in which the “end of history” is not a benevolent Engelsian settlement but a permanently unstable balance between creative destruction, political backlash, technocratic patch‑up, and ideological re‑framing. Engels, standing in a steam‑powered mill in 1870, could see the old order dying. He could not, I think, quite see the strange new order being born in its place.

2026-04-28 17:00-18:30 BST (Tue): <https://zoom.us/j/8458651578?omn=95983788025>

Meeting ID: 845 865 1578

Passcode: 764724

If reading this gets you Value Above Replacement, then become a free subscriber to this newsletter. And forward it! And if your VAR from this newsletter is in the three digits or more each year, please become a paid subscriber! I am trying to make you readers—and myself—smarter. Please tell me if I succeed, or how I fail…

##fyi-theories-of-eeconomic-history

##lecture-notes

##enlarging-the-scope-of-human-empire

#2026-hicks-lecture

#economic-history

#grand-narrative

#stage-theory

#john-hicks

#oxford-lecture

#institutional-change

#technological-change

#macro-history

#global-economy

#theories-of-economic-history

<https://braddelong.substack.com/t/theories-of-economic-history>